“Mr. Spock, the women on your planet are logical. That’s the only planet in the galaxy that can make that claim.” – Captain Kirk

This post has taken far longer for me to put together than I had anticipated. I spent quite a bit of time putting together the data and moving down paths that didn’t work. It is also taking more text & space than I had anticipated. Therefore I am splitting this into multiple posts. This first post covers the explosion of assets in yield bearing equities. One last editorial note, substitute “investors” for women in the quote above.

In at least on respect, FED policy is working: QE via its bond buying program is forcing investors up the risk curve. And that is making for an unintentionally very over-crowded trade. This is because multiple trends are coming together into the same or similar assets due to investors’ search for yield and safety. It is the natural reaction investors have to getting burned twice before reaching for capital gains: first in 2000 with dotcoms and in 2008 in real estate. Rather than seek capital gains, they are trying to play it safe by being content to collect dividends. But investors are paying high prices for small cash flows and the quest for yield is playing out in bulk. If this plays out as another crash as I expect it will, the irony will be that investors were trying to be conservative.

Here are some of the trends:

– Dividend stocks

– REITs

– MLPs

– Preferred stocks

– Low-volatility investing

– Risk parity investing

– Yen depreciation

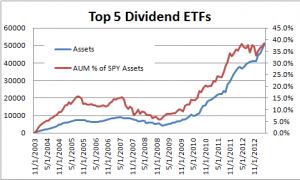

It’s easy to see how a quest for yield leads investors to these first four sectors of the stock market. Even bond investors seem to be getting into the act. There is an enormous amount of money chasing these sectors and the data to support that follows. First, consider dividend paying stocks. I’ve put together data on fund assets under management (AUM) for the top 5 dividend ETFs. These account for the vast majority of dividend ETF assets. Of course, mutual fund assets are larger, but this data should capture the money flow trends. The chart shows the hockey stick growth of assets both on an absolute basis and compared to SPY assets. When looking at the percentage figures, keep in mind that SPY assets have also grown aggressively recently, having increased by over 28% in the past year and most of that, 21%, in the past 6 months. That’s not bad for a fund that a year ago had $100B.

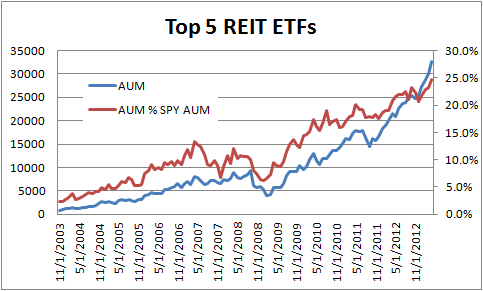

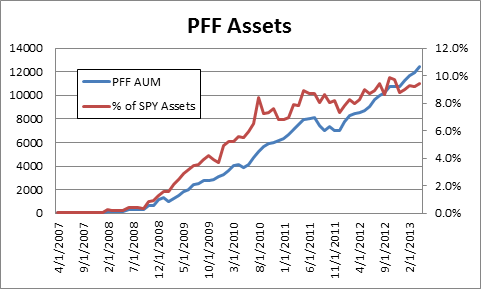

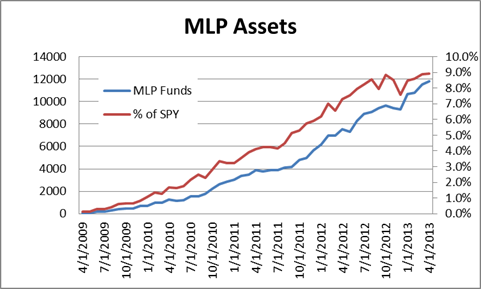

Overall, the top 5 dividend ETF assets has exploded in the past two years to over $50B (incidentally higher than that managed by GLD) – managing 4X the assets as at the end of 2010. Chart data from Bloomberg. REIT ETFs have doubled in size since the end of 2010 from a sizable asset base of $14B. PFF accounts for so much of the preferred ETF market that it is the only fund that I listed. It, too, has more than quadrupled its assets since the end of 2010. MLP assets have grown very quickly to become nearly $12B.

Clearly, an incredible amount of money has been rushed into these yield related stocks in the past two years – just in ETFs alone. But it gets more interesting. Although low volatility investing as a concept has been around for some time, it has recently become very popular. Consider that SPLV, the leading low volatility(LV) ETF, launched in May 2011 and already with over $5B in assets. SPLV’s largest competitor, USMV, was launched October 2011 and now has $3.5B. The Top 5 low volatility ETFs combined are managing $12.6B which is about 9.5% of the size of SPY. These funds have been in such demand that their assets have more than doubled this year (all 5 months of it).

Certainly there is significantly more money than this in the mutual fund complex and under non-categorized active management following low-volatility strategies. But the kicker here is that these low volatility funds look a lot like their dividend ETF competitors. First, they are very heavily weighted in the consumer (combined consumer staples & discretionary) with weightings around 20%, very comparable with dividend funds that have slightly higher concentrations in the mid-20%s and also the SPX. They have higher than SPX weightings in utilities, with dividend ETFs having a typically very heavy 10-30% (with Vanguard having 1%) and LV ETFs having between 9-30% weightings, compared with 3.3% for the SPX. LV ETFs are also very heavily weighted in real estate (including REITs). SPLV accounts for nearly half of LV ETF assets and holds 10% in real estate and the next two holding 7% and 2% respectively vs. 2% for SPX.

Another new, but prevalent trend in investing is called risk parity investing. The idea is, roughly speaking, to allocate assets in a portfolio such that each asset class’s variability (risk) is equal. For example, bonds typically have lower volatility than equities, thus the bond allocation would be levered up until the new allocation had a perceived volatility equivalent to the equity component. Each manager handles this slightly differently. But they might lever up on low volatility equity sectors to match, say, technology shares or the market as a whole. Frankly, it is beyond my capabilities at this time to provide a reasonable metric on how much money is involved in risk parity. There is an interesting discussion about it here and an article here. My feeling is that there are large amounts of assets put to work in this way, but I prefer data to feelings. Input would be very welcome.

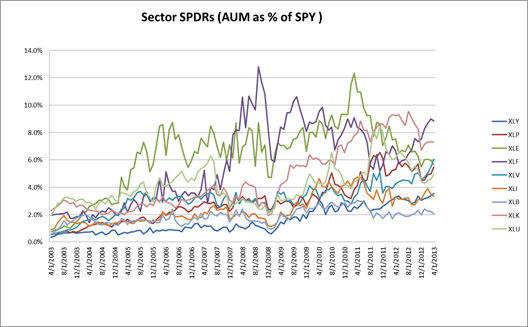

To provide a more complete picture, take a look at this next chart that shows Sector SPDR assets as a percentage of SPY assets. This shows that prior data was not documenting a secular decline in SPY assets relative to other ETFs. One can see that on a relative basis that some sectors have gathered assets and other lost. In particular, it is worth noting that the utilities sector (XLU) has seen a recent and dramatic drop in assets. This is a bit odd since utilities are the poster boy for dividend stocks. It might mean that investors wanted to diversify into a number of dividend payers, presumably for risk reduction. However, recall that utilities represent a significant part of dividend ETF portfolios and the dividend ETFs are far larger than XLU so that even that fraction (as high as 30%) can easily offset (relative) outflows from XLU.